Unlocking Africa's Most Complex Economic Frontier

by LSIG Economic Development Team

5/6/202612 min read

Agricultural zones. Inter-provincial trade flows. Intra-African trade. International trade dynamics.

A Strategic Landscape Analysis for Investors, Governments & Development Partners

Country Profile: A Giant with Untapped Potential

Geography & Natural Capital

The DRC is the second-largest country in Africa by area (2,345,410 km²) and is geographically diverse in ways that directly shape its economic potential. Its territory spans the Atlantic coast in the west, the equatorial rainforest basin in the north — one of the largest in the world — montane highlands bordering the East African Rift, and savanna zones in the center and south. It shares borders with nine countries, positioning it as a natural hub for Central and East African trade.

Key natural assets include:

• Over 80 million hectares of arable land (less than 40% currently under cultivation)

• More than 50% of Africa's freshwater reserves, including the Congo River, Lakes Tanganyika and Kivu, and extensive groundwater systems

• Critical mineral deposits: cobalt, copper, lithium, manganese, and phosphate, essential inputs for global green energy and electronics supply chains

• Virunga National Park, Africa's oldest national park, and rich biodiversity assets

Minerals, Rare Earths & the Green Economy Connection

By 2025, the DRC's strategic importance in global supply chains has intensified significantly. Its critical mineral reserves, particularly cobalt (the DRC supplies over 70% of global production) and lithium, are indispensable to electric vehicle batteries, renewable energy storage, and consumer electronics. For investors with long-term supply chain mandates, the DRC represents a primary sourcing node.

$192.2 billion rise

in intra-Africa trade, representing a 3.2% increase from previous year

$56.4 billion

total goods traded in 2025 between U.S. and Sub-Saharan Africak

Executive Summary

Today’s global business environment is being reshaped by shifting trade alliances, changing tariff policies, regional conflicts, and increasing geopolitical complexity. While uncertainty continues to influence markets, one constant remains: organizations and nations worldwide are still pursuing growth, expansion, and strategies that generate sustainable, long-term returns on investment.

Across Africa, a powerful transformation is underway. Countries are accelerating intra-African trade while prioritizing local value addition and industrialization.

For instance, Côte d'Ivoire, one of the world’s two largest cocoa producers, has made significant progress in moving up the value chain. Since 2010, it has ranked alongside Netherlands as a leading global hub for cocoa processing, according to recent industry reports. With projected GDP growth rising from 6.0% in 2024 to 6.5% in 2025, Côte d’Ivoire remains one of the fastest-growing economies in Francophone Africa.

Beyond agriculture, the country is strategically investing in tourism through its flagship “Sublime Côte d’Ivoire” initiative (2018–2025), which has now evolved into a long-term national ambition. The program aims to attract 5 million international visitors annually by focusing on business tourism, eco-tourism, and the development of its 550-kilometer coastline. By linking investment attraction to hospitality infrastructure, the initiative is expected to generate over 700,000 jobs while driving investment in hotels, resorts, and tourism training.

Similarly, Ghana, another global cocoa producer powerhouse, is advancing its position in the value chain by expanding into domestic chocolate manufacturing, signaling a shift from raw commodity export to finished goods production. At the same time, the country which has historically exported raw gold to destinations such as South Africa for processing, is undertaking a major policy shift to ensure that a greater share of its gold is refined domestically through new agreements with the Gold Coast Refinery. Backing from South Africa’s Rand Refinery, an LBMA-accredited refiner, further strengthens credibility and signals confidence in Ghana’s ability to meet strict international standards.

Also, Republic of Benin is actively advancing a set of strategies aimed at positioning the country as a leading investment destination. A notable milestone is the launch of the Glo-Djigbé Industrial Zone (GDIZ), a major industrial hub for manufacturing and agro-processing in Francophone Africa, established through a public-private partnership between Arise Integrated Industrial Platforms, founded by Indian businessman named Gagan Gupta, and the Beninese government.

In 2024, GDIZ began exporting “Made in Benin” ready-to-wear cotton garments, marking a significant shift from raw cotton exports toward local value addition. The zone also supports the processing of key agricultural commodities, including cashew nuts.

Beyond industrialization, Benin is strengthening its role as a regional trade partner. The country is increasingly exporting vegetable residues (valued at $2.18 million in 2024) and cashews to South Africa, while also serving as a critical logistics and transit corridor for landlocked countries such as Chad, Burkina Faso and Niger, facilitating the movement of goods across the region.

Moreover, across the continent, intra-African trade is already delivering tangible results. Tanzania has successfully exported coffee to Algeria and sisal fiber to Nigeria, signaling a shift beyond raw commodity exports toward more processed, market-ready products.

In parallel, amid ongoing global energy pressures, many African as well as European countries are increasingly looking to Nigeria’s refining capacity as a strategic solution to meet regional demand for refined petroleum products.

These examples underscore a broader reality: Africa is far more than the narrative of conflict or humanitarian challenges often portrayed. The continent represents a vast agricultural powerhouse and an increasingly strategic hub for value creation and industrial growth.

At the same time, the Democratic Republic of the Congo (DRC) stands at a critical economic inflection point. With its vast natural resources and strategic position in global supply chains, the country holds significant potential to shape the next phase of Africa’s economic transformation.

Endowed with extraordinary natural wealth, from the world's second-largest tropical forest and 80 million hectares of arable land to more than 50% of Africa's fresh water reserves and an unparalleled concentration of critical minerals, the DRC presents a rare convergence of resource abundance and structural underdevelopment that, for discerning investors and development partners, translates into outsized opportunity.

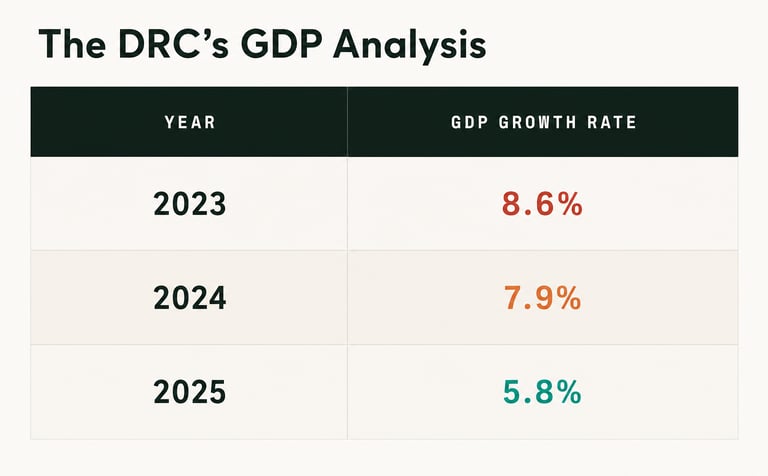

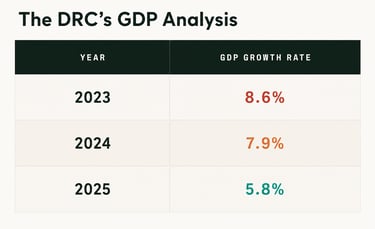

Economic growth has remained strong in recent years (8.6% in 2023, 7.9% in 2024), though it decelerated to 5.8% in 2025. This slowdown, however, reveals an important signal: the economy remains overly dependent on extractive industries, while agriculture sub-branch, secondary sector (such as electricity, construction…), and tertiary sector (trade, transport…), sectors with the most room for private-sector impact, remain severely undercapitalized. The gap between what the DRC produces and what it could produce is not a risk factor; it is the investment thesis.

This case study maps the DRC's growth dynamics, identifies structural gaps, highlights key agricultural zones and trade corridors, and outlines strategic entry points for LSIG clients across agriculture, logistics, agro-processing, cold chain infrastructure, and industrial development.

$1.9B

Food & agricultural imports in 2024, in a country with 80M ha of arable land

LSIG Client Relevance

Clients in clean energy, EV manufacturing, electronics, or mineral processing have a direct strategic interest in DRC market entry, partnership structures, and supply chain assurance mechanisms.

Growth Dynamics: Performance & Structural Fragility

Macroeconomic Trajectory

The DRC's recent growth record reflects a resource-driven economy operating well below its productive ceiling:

Other estimates, including those from the World Bank, indicate that the 2025 growth rate stood at 5.5 percent, from 6.1 percent in 2024.

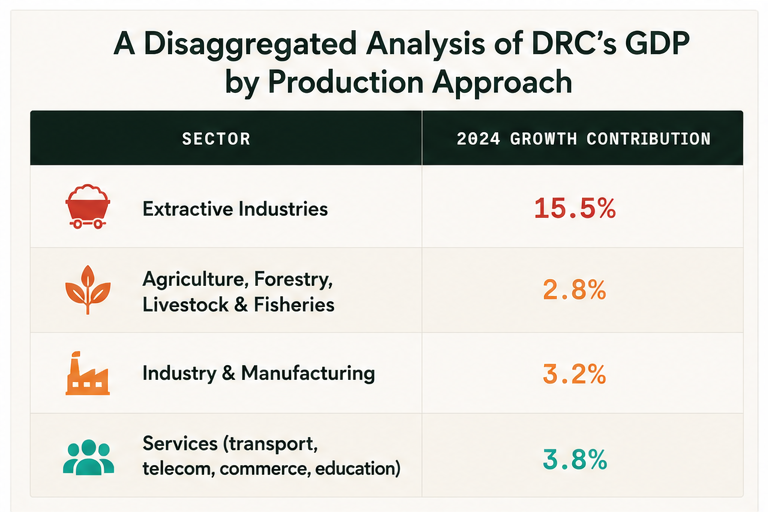

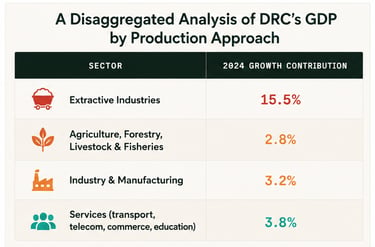

Sectoral Breakdown: Where Growth Comes From and Where It Could Come From

A disaggregated analysis of GDP by production approach reveals a growth structure that is both concentrated and fragile:

Economic growth continued to be driven by the extractive sector, particularly strong copper production and exports, although overall momentum slowed. Mining growth declined from 11.9 percent in 2024 to 10.1 percent in 2025, while non-mining sectors grew by 3.1 percent, supported mainly by construction and services. The slowdown was largely attributed to the temporary cobalt export ban (between February and October 2025) led to a sharp decline in cobalt export volumes, but also to the ongoing insecurity linked to the M23 armed group in the mineral-rich eastern regions and increased defense spending.

Strategic Insight for LSIG Clients

A 2.8% agricultural growth rate in a country where fewer than 40% of arable lands are cultivated is not a sector weakness, it is an artificial ceiling created by infrastructure and investment gaps. Private capital can directly lift it. Clients entering agricultural transformation, logistics, regional processing, distribution infrastructure, agro-processing facilities, cold storage, and distribution logistics or agribusiness services are targeting exactly the sectors where the margin for progress is highest and competition lowest.

The Import Paradox: A Country Feeding Itself from Abroad

Perhaps the most striking signal of structural underperformance is DRC’s food import dependency. The country that holds some of Africa's most fertile land is a net food importer:

• Food and agricultural imports exceeded 1.9 billion USD in 2024, with key imports such as rice, poultry, dairy, palm oil, wheat, and vegetables

• Zambia's National Food Reserve Agency (NFRA) committed to exporting 1 million tonnes of maize to the DRC in FY2025/2026 — including to Kasaï provinces that have significant agricultural capacity of their own

• The country was recently dependent on maize imports from Zambia and South Africa despite its strong local production base

This paradox — fertile land, chronic food insecurity — is a direct consequence of insufficient post-harvest infrastructure, cold chain gaps, poor inter-provincial road connectivity, and limited processing capacity.

Each of these represents a concrete investment opportunity.

Agricultural Landscape: Key Zones & Commodities

The DRC's agricultural potential is geographically distributed across distinct agro-ecological zones, each with specific commodity profiles and market linkage needs:

Kwilu

Key commodities: Cassava, maize, groundnuts, soybeans, paddy rice, cowpea

Kasaï Central & Kasaï Oriental

Key commodities: Maize, beans, pineapple, paddy rice, groundnuts, coffee, palm oil, cassava

South Kivu, North Kivu & Tshopo

Key commodities: Coffee, cocoa, colocasia, beans, rice, maize, sweet potato, banana, onion, tomato, tea, palm oil, dairy, cassava, sorghum, potato

Ituri, Haut-Uélé & Bas-Uélé

Key commodities: Rice, maize, palm oil, cocoa, coffee, cassava, sweet potato, groundnuts, plantain, timber

Haut Katanga, Haut Lomami & Lualaba

Key commodities: Maize, cassava, groundnuts, beans, sweet potato, rice, soybeans, palm oil, market gardening

Équateur & Mongala

Key commodities: Palm oil, rice, cocoa, cassava, maize, plantain, groundnuts, mushrooms

Livestock farming and fishing are also present across nearly all provinces, adding protein supply chain opportunities.

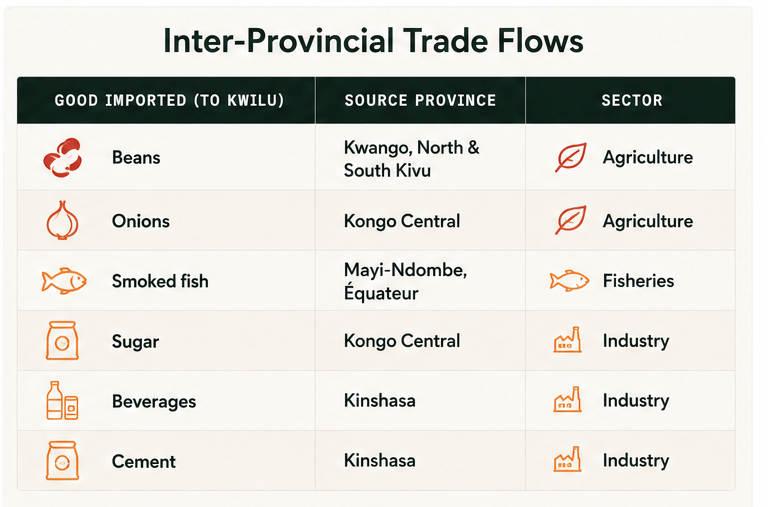

Inter-Provincial Trade Flows: Evidence of Commercial Connectivity Gaps

Existing inter-provincial trade data reveals patterns that highlight both the dysfunction and opportunity in domestic supply chains. For example, Kwilu province, itself an agricultural producer, is importing basic goods from other regions:

Similar inter-provincial trade flows are observed across all the provinces. For example, Kasaï-Central import cement, vegetable oil, beverages, sugar, semolina, and canned fish primarily from Kinshasa, despite having local agricultural capacity.

Food Security Paradox

Despite its agricultural endowment, the DRC has been classified under IPC categories for acute food insecurity, acute malnutrition, and chronic food insecurity since 2014. This is not a resource scarcity problem, it is an infrastructure, logistics, and institutional failure that private investment can structurally address.

Program-Level Governance Challenges

Numerous stakeholders in Africa advocate for a new approach to financing, program design, and risk mitigation in order to effectively strengthen the agricultural sector in Africa. In fact, the following factors have been identified and can serve as a foundation for strategic reflection and opportunity development for entrepreneurs and investors:

• Workshops and policy dialogues rarely translate into implementable, on-the-ground change

• Poor coordination between organizations, donors, and government ministries

• Limited agro-financing literacy among financial institutions

• Weak monitoring and evaluation mechanisms for agricultural programs

• Insufficient support for family farming, which remains the backbone of food production

Trade & Investment Environment

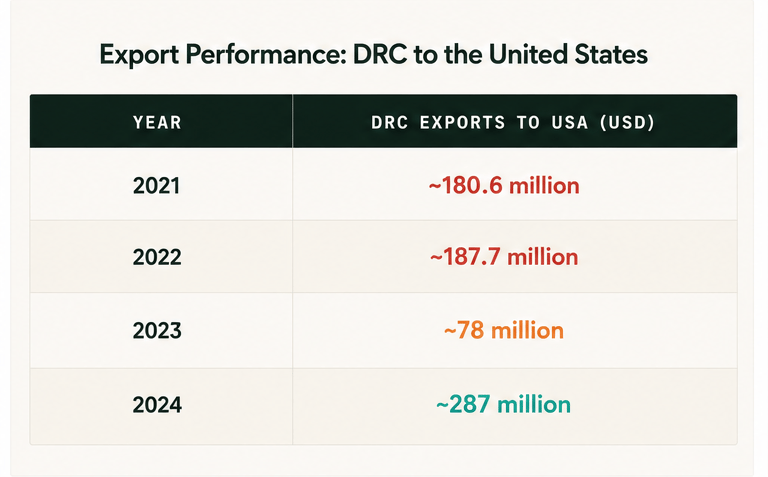

Export Performance: DRC to the United States

The 2024 export surge — driven by textiles, processed agricultural goods, and semi-processed raw materials — reflects the early benefits of product diversification. North Kivu's coffee, cocoa, and palm oil also carry strong organic/bio export potential to both the EU and US markets.

Import Outlook: The United States to DRC

In 2024, U.S. exports to the Democratic Republic of the Congo totaled $240 million, led by $54.5 million in cereal meals and pellets, followed by $29.1 million in poultry and $23.8 million in dried legumes.

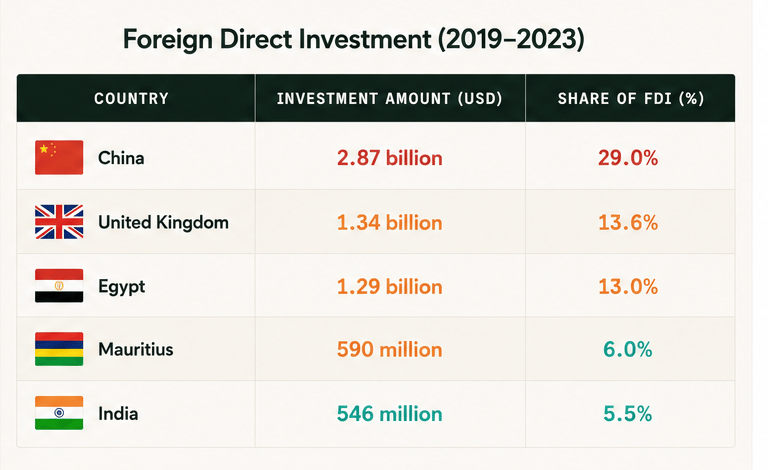

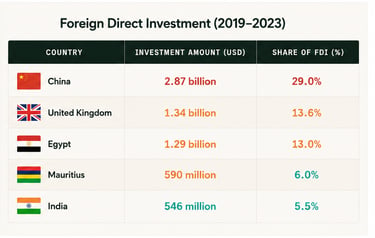

Foreign Direct Investment (2019–2023)

Total FDI of 13.56 billion USD was channeled through 386 projects approved by ANAPI (Agence Nationale pour la Promotion des Investissements) during this period. Key data:

• FDI accounted for 72.9% of total investment (approx. 9.89 billion USD)

• Sector breakdown: Services 44.8% | Industry 40.7% | Infrastructure 8.5% | Agriculture 5.9%

As of 2026, the UAE, through DP World, is developing DRC first deep-water port at Banana, aimed at transforming regional trade with a 30-year concession.

LSIG Observation

Agriculture received only 5.9% of total FDI despite accounting for a dominant share of employment and food security needs. This structural mismatch between investment allocation and economic need is a defining opportunity for mission-aligned and commercially motivated investors alike.

Special Economic Zones (SEZs): Potential & Policy Gaps

The DRC government has defined six major industrial clusters for SEZ development, overseen by the Agence des Zones Économiques Spéciales (AZES). Seven SEZs have been designated (Maluku, Kin-Malebo, Kiswishi, Kinsevere, Musompo, Sud-Ubangi, and Musiénene), with four currently operational.

Notable SEZ: Kiswishi — A Private-Sector Model

Kiswishi stands out as the DRC's first privately piloted SEZ, managed by a subsidiary of the Rendeavour Group. It operates across two verticals: real estate and industrial. Kiswishi represents a template for private-sector-led zone development that could be replicated across the country's agricultural heartlands.

Policy Recommendations for SEZ Optimization

• Reorient SEZ strategy toward domestic value-added production (inter-provincial supply chains) rather than export-first models, especially given current geopolitical volatility

• Deliberately site new SEZs in high-potential agricultural zones, not just near urban centers or export corridors

• Adopt long-term land lease models for SEZ land rather than outright acquisition, to ensure fair benefit-sharing with local communities

• Require community relocation plans with long-term compensation frameworks, not one-time payments, to prevent reputational and social risks for investors

Private Sector Landscape: Key Players

The DRC hosts a diverse agro-industrial private sector spanning large conglomerates to innovative SMEs:

Groupe LEDYA (Large Enterprise)

A diversified conglomerate with operations spanning transport, consumer goods distribution, hospitality (3 major hotels), ports & logistics (TICOM), petroleum (Lerexcom Petroleum, Ledya Oil and Gas DS), mining (copper, cobalt, manganese), and real estate. LEDYA illustrates the vertically integrated model that major investors may use to navigate the DRC's complex commercial environment.

ETS MWINJA (SME / Local Innovation)

Ets Mwinja, a locally driven and innovative company that has successfully transitioned from a small and medium-sized enterprise (SME) to a large-scale business, originated as a supplier of industrial and construction materials, expanding over time into a multi-sector company, with operations spanning cement, petroleum, land transport, and more recently, the production and commercialization of bottled drinking water.

Structural Challenges & Risk Landscape

Infrastructure Deficit

• Road and rail networks are severely degraded. The SNCC (national rail operator) functions at less than 5% of its rated capacity

• Poor inter-provincial connectivity increases logistics costs and creates market fragmentation

• Cold chain infrastructure is nearly absent in most provinces, leading to significant post-harvest losses (estimated 5–10% for perishables like tomatoes in East DRC)

Energy Gap

Reliable electricity remains a critical constraint for industrial and agro-processing activity. Public infrastructure includes Inga I & II and the Ruzizi I & II hydroelectric plants (operating below capacity) and the Tshopo plant (Unit 1 restored in January 2026). The private sector is beginning to fill the gap:

• Virunga Energies: hydro-based private supply

• Énergie du Nord-Kivu (ENK) : regional energy provider

• Nuru, Bboxx, GoShop: solar energy operators

Strategic Opportunities for LSIG Clients

Based on this landscape analysis, LSIG has identified several entry points that closely align the Democratic Republic of the Congo’s structural gaps with LSIG's client capabilities; however, only a select number of opportunities will be presented here.

For instance, infrastructure development stands out as a priority opportunity. The rationale is to modernize core infrastructure in order to strengthen intra-provincial trade flows while reducing the country’s heavy dependence on food imports. A viable entry mechanism for this area could include public-private partnership (PPP), and joint ventures models.

Similarly, agro-processing and value-added manufacturing present a compelling opportunity, given that less than 40% of arable land is currently cultivated and there is limited domestic processing capacity for key commodities. Entry mechanisms in this space could include joint ventures, special economic zone (SEZ) licensing, warehouse development, and anchor tenant models.

Conclusion: The DRC Investment Analysis - The Gap IS the Opportunity.

The Democratic Republic of Congo is not a frontier market in the conventional sense of the term. It is a structured opportunity landscape where the size of the gap between current performance and potential performance is itself the investment case. Its minerals are globally indispensable. Its agricultural land is among the most fertile in the world. Its water resources are unrivaled on the continent. And its food insecurity, infrastructure deficit, and processing gaps are paradoxically the signals that should attract sophisticated, patient capital rather than deter it.

For LSIG clients with a mandate in economic development, supply chain resilience, or emerging market growth, the DRC presents rare alignment: high impact, high return potential, and low competition in the sectors that matter most.

The question is not whether the DRC can deliver returns. It is whether investors are structured to navigate the complexity and whether they enter now, while the landscape is still being defined.

From Insight to Investment

For governments, investors, development partners, entrepreneurs and institutions, the message is clear: the opportunity is not only in entering African markets but in entering them strategically and growing steadily.

Capturing value in today’s environment requires more than capital deployment. It demands:

Deep, data-driven understanding of local markets

Alignment with national development priorities

Strong risk assessment and mitigation frameworks

Integrated approaches that connect sectors such as agriculture, infrastructure, and tourism

This is where LSIG (Leo Strategic Innovation Group) plays a critical role.

We partner with our clients to move beyond surface-level market entry and toward high-impact, sustainable investment strategies. From economic and sector diagnostics to portfolio performance analysis, investment corridor mapping, and program evaluation, LSIG equips decision-makers with the intelligence needed to act with confidence in complex environments.

Now is the time to act.

Organizations that position themselves early while aligning strategy with local transformation agendas will define the next generation of market leaders across Africa.

Engage with LSIG to:

Identify high-potential investment opportunities

De-risk your portfolio through rigorous analysis

Design and monitor programs aligned with long-term impact and returns

Translate strategy into measurable, sustainable performance

Africa’s transformation is underway. The question is no longer whether to engage but how to engage effectively.

Sources: BCC, ANAPI, CESCN, AZES, ANAPI/AD'OCC, IPC, Kiala (2025), Amedee (2025/2026), BANKABLE (2024), CAID, greenafia (2025), Brookings (January 2025) , US Trade Representative, SpotlightinAfrica (2026), OEC -The Observatory of Economic Complexity, U.S. Department of State, LSIG Economic Development (2025), World Bank.

LSIG's Economic Development practice helps investors, development partners, institutions and government agencies navigate complex markets through rigorous landscape analysis, investment corridor mapping, and program evaluation.

CONNECT:

© 2026. All rights reserved.

LSIG

HELPFUL LINKS

TERMS OF USE

COMPANY